Vacant Land New Listing

If one of the goals on your list is selling your house and making a move this year, you’re likely juggling a mix of excitement about what’s ahead and feeling a little sentimental about your current home.

A great way to balance those emotions and make sure you’re confident in your decision is to keep these three best practices in mind when you’re ready to sell.

The housing market shifted in 2023 as mortgage rates rose and home price appreciation started to normalize once again. As a seller, you still need to recognize how important it is to price your house appropriately based on where the market is today. Hannah Jones, Economic Research Analyst for Realtor.com, explains:

“Sellers need to become familiar with their local market and work closely with a local agent to make sure their listing is attractive to buyers. Buyers feeling the pressure of affordability are likely to be pickier, so a well-priced, well-maintained home is the ticket to drumming up big demand.”

If you price your house too high, you run the risk of deterring buyers. And if you go too low, you’re leaving money on the table. An experienced real estate agent can help determine what your ideal asking price should be, so your house moves quickly and for top dollar.

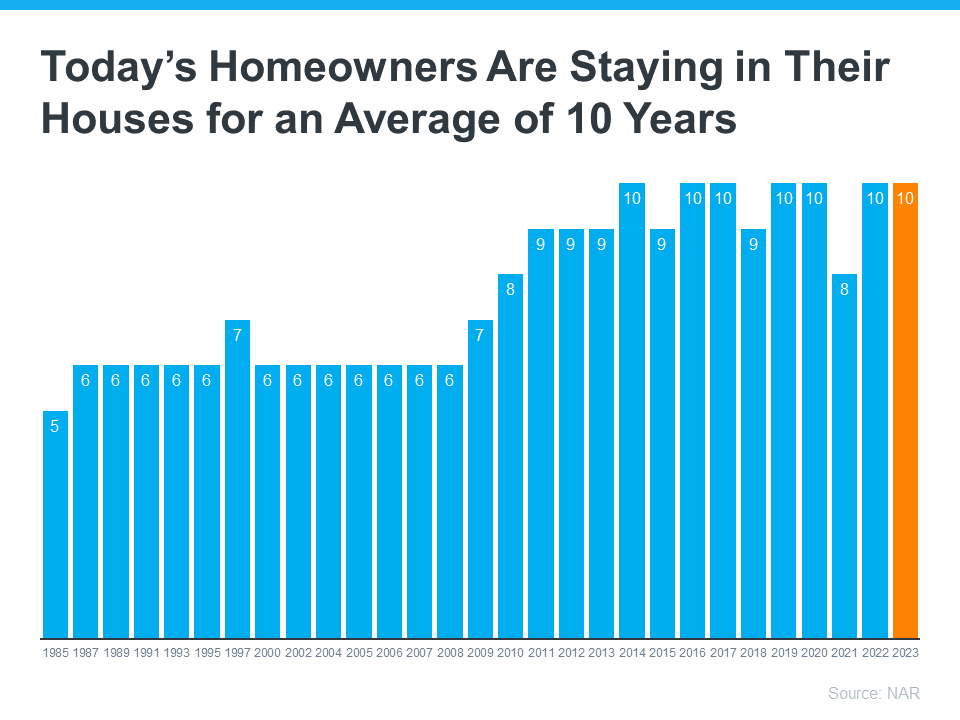

Today, homeowners are staying in their houses longer than they used to. According to the National Association of Realtors (NAR), since 1985, the average time a homeowner has owned their home has increased from 6 to 10 years (see graph below):

This is much more than what used to be the norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you bought or the house where your loved ones grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from the sentimental value.

For some homeowners, that makes it even tougher to separate the emotional value of the house from fair market price. That’s why you need a real estate professional to help you with the negotiations and the best pricing strategy along the way. Trust the professionals who have your best interests in mind.

While you may love your decor and how you’ve customized your house over the years, not all buyers will feel the same way about your vibe. That’s why it’s so important to make sure you focus on your home’s first impression, so it appeals to as many buyers as possible.

Buyers want to be able to picture themselves in the home. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. As Jessica Lautz, Deputy Chief Economist and Vice President of Research at NAR, says:

“Buyers want to easily envision themselves within a new home and home staging is a way to showcase the property in its best light.”

A real estate professional can help you with expertise on getting your house ready to sell.

If you’re considering selling your house, let’s connect so you have help navigating the process while prioritizing these must-do’s.

Take a look at the December 2023 Snapshot . The median days for a home on the market was 22 days, the average sale price was $575,000, and cost per square foot was $350. If you are interested in becoming a homeowner or selling a home in 2024, let us guide you through the process. We look forward to hearing from you in the new year and are here to work together with you!

If buying or selling a home is your goal for 2024, it’s important to understand today’s housing market, know your why, and work with industry experts to bring your homeownership vision for the new year into focus.

Over the last year, the economy had a big impact on the housing market, and likely on your wallet too. That’s why it’s critical to have a clear picture of not just the market today, but also on what you want out of it when you buy or sell a home. Danielle Hale, Chief Economist at Realtor.com, explains:

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, so that you can stay in your home long enough that buying is a sound financial decision.”

Here are a few things to think through as you define your goals for 2024.

You’re dreaming about making a move for a reason – what is it? No matter what’s happening in the market, there are still many compelling reasons to buy a home today. Your needs may have changed in a way your current house can’t address, or you could be ready to step into homeownership for the first time. Use your why and your motivation as a guidepost in partnership with an expert advisor to make sure your move gives you a lasting sense of accomplishment.

You know you want to move, but how would you describe your dream home? The number of homes for sale has grown recently, and that could mean more options to choose from when you buy. But overall housing supply is still lower than more normal years in the market, so you’ll have to work closely with a pro to find what you’re looking for. Just be sure to keep your budget in mind as you balance your wants and needs. The better you understand what’s essential and where you can be flexible, the easier it will be to find a home that’s right for you.

Getting clear on your budget and available savings is essential before you get too far into the process. Partnering with a local agent and a lender early is the best way to make sure you’re in a good position to buy. This could include planning how much to save for a down payment, getting pre-approved for a home loan, and assessing your current home equity if you’re selling your existing house.

Buying or selling a home takes expertise to navigate. If that feels a bit overwhelming, that’s normal. Don’t let uncertainty hold you back from your goals this year. A trusted expert will help you bridge that gap and give you the facts and advice you need about today’s housing market.

Let’s connect to plan how to make your homeownership dreams a reality in 2024.

Even with so much data showing home prices are actually rising in most of the country, there are still a lot of people who worry there will be another price crash in the immediate future. In fact, a recent survey from Fannie Mae shows that 23% of consumers think prices will fall over the next 12 months. That’s nearly one in four people who are dealing with that fear – maybe you’re one of them.

To help ease that concern, here’s what the experts say will happen with home prices not just next year, but over the next five years.

While seeing a small handful of expert opinions may not be enough to change your mind, hopefully, a larger group of experts will reassure you. Here’s that larger group.

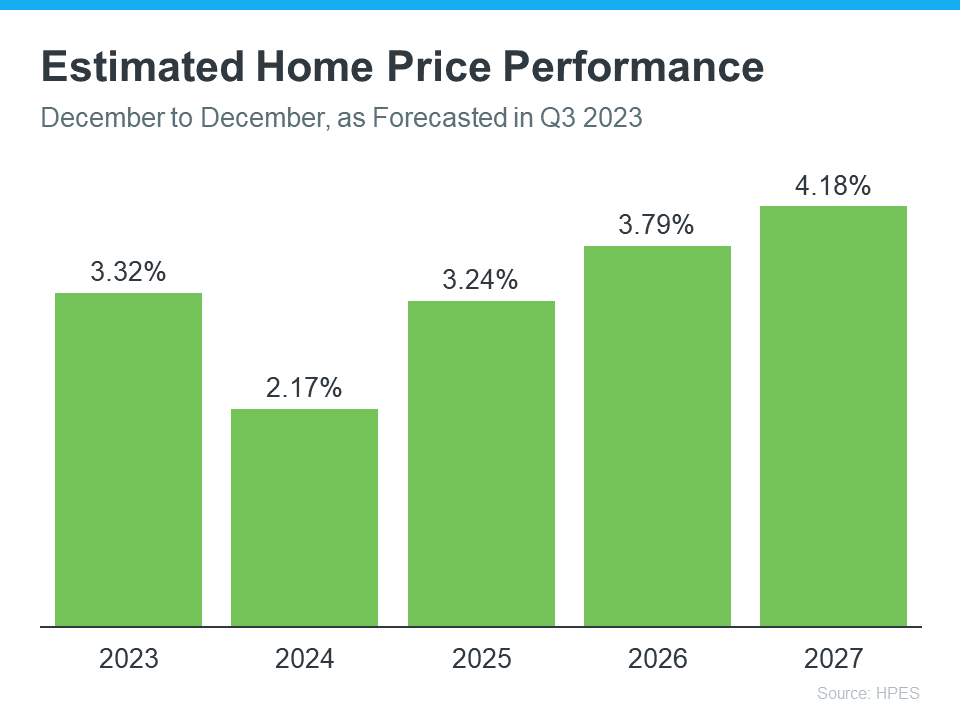

The Home Price Expectation Survey (HPES) from Pulsenomics is a great resource to show what experts forecast for home prices over a five-year period. It includes projections from over 100 economists, investment strategists, and housing market analysts. And the results from the latest quarterly release show home prices are expected to go up every year through 2027 (see graph below):

And while the projected increase in 2024 isn’t as large as 2023, remember home price appreciation is cumulative. In other words, if these experts are correct after your home’s value rises by 3.32% this year, it should go up by another 2.17% next year.

If you’re worried home prices are going to fall, here’s the big takeaway. Even though prices vary by local area, experts project they’ll continue to rise across the country for years to come at a pace that’s more normal for the market.

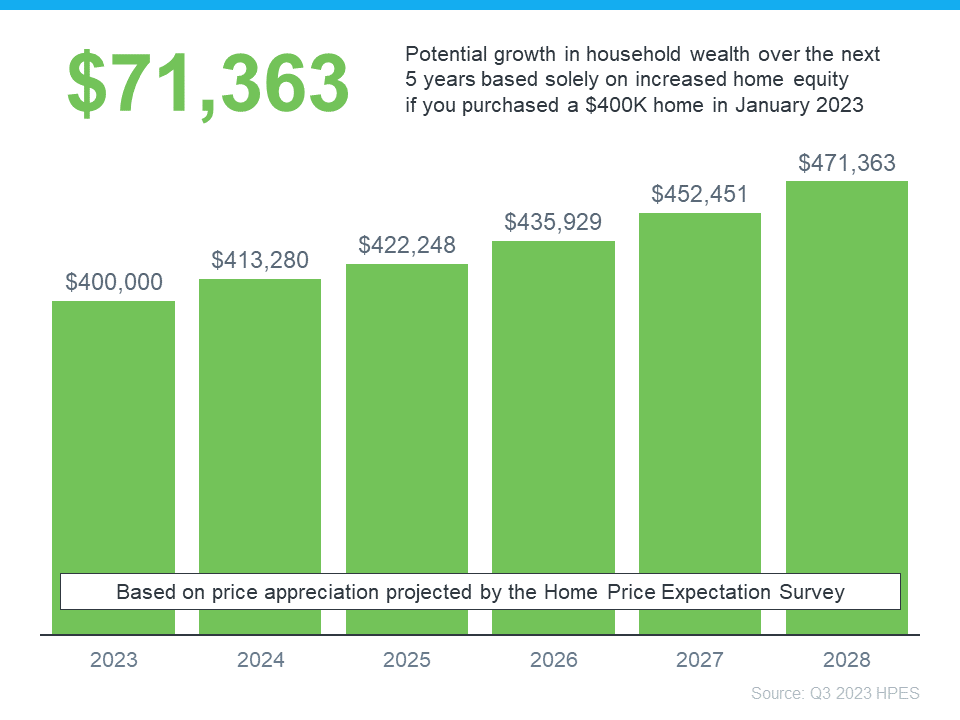

If you’re not convinced yet, maybe these numbers will get your attention. They show how a typical home’s value could change over the next few years using the expert projections from the HPES. Check out the graph below:

In this example, let’s say you bought a $400,000 home at the beginning of this year. If you factor in the forecast from the HPES, you could potentially accumulate more than $71,000 in household wealth over the next five years.

If you’re someone who’s worried home prices are going to fall, rest assured a lot of experts say it’s just the opposite – nationally, home prices will continue to climb not just next year, but for years to come. If you have any questions or concerns about what’s next for home prices in our local area, let’s connect.

The Lynden housing market for October: Median sales price increased 2% year over year, average days on market more than doubled, and inventory climbed nearly 50%.

If your goal is to get into a new home by the end of the year, let’s connect to get the ball rolling now! We would love to help make that happen for you.